NB: Preliminary results as at 20 April 2020

Summary

Sakeliga is currently conducting an ongoing survey to determine the impact of Covid-19 and current disaster management regulations. Unfortunately, as was the case in our first survey, the results of our second survey are still not good news for business.

Feedback from Sakeliga’s membership base and broader network still indicates an extremely challenging time for many businesses and a severe deterioration of immediate business conditions. Most respondents in our survey are involved in businesses with fewer than 50 employees, and from the results, we deduce that the impact of Covid-19 on small and medium enterprises is considerable. Although there are potential minor positives compared to our first survey, future prospects for business, even after 12 months, are mostly still negative and uncertain.

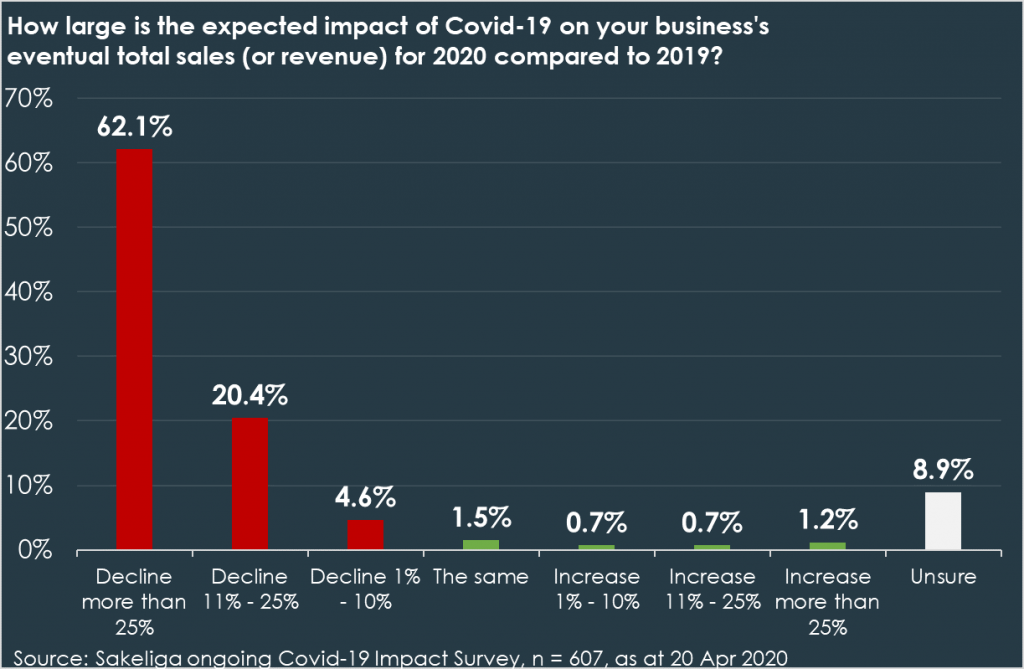

It is especially worrisome is that almost two-thirds of all participants who completed our questionnaire indicated an expected decline in revenues (or total sales) of more than a quarter (or 25%) for 2020.

We are also seeing that almost a third of respondents indicate that their companies have been appointed as “essential” under the Covid-19 regulations. From these 180 respondents in “essential” businesses, about half indicated that it is currently tougher than usual to obtain the necessary inputs for operations. For three out of four of those in “essential” businesses, it is much more difficult or somewhat more difficult to obtain the necessary production inputs. This situation confirms concerns even from essential businesses about access to and availability of the inputs they need for their operations.

Results in a nutshell

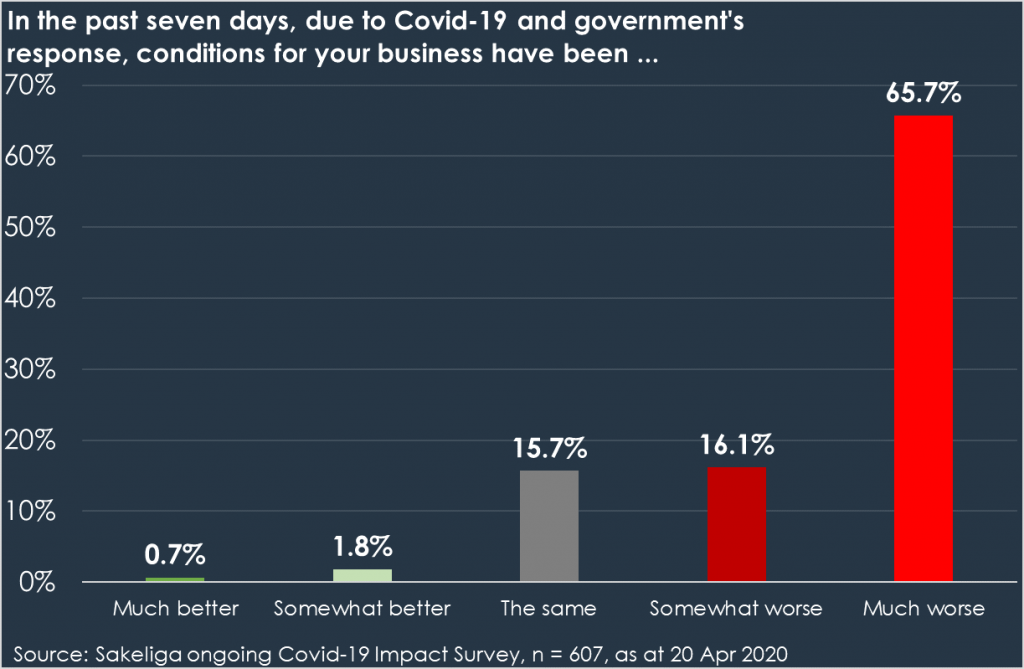

- Sakeliga’s recent survey revealed that for 82% of respondents that took part in the survey, current conditions have significantly deteriorated due to the Covid-19 crisis. 66% indicated that conditions have deteriorated considerably and for 16% they deteriorated to some extent. We are definitely still seeing a severe immediate impact on businesses.

- We are still seeing that a minority of respondents are expecting better prospects than before. This remains the case over 30 days, 90 days and even after 12 months, although the 12-month outlook is somewhat better.

- Significant uncertainty about the future is indicated, and uncertainty seems to increase the farther people look into the future.

- Few respondents thought that their businesses would eventually be able to largely offset the damage of Covid-19.

- Nearly two-thirds of the respondents expect a decline of more than 25% in revenue or total sales in 2020.

- About a third of the respondents indicated that their company has been designated as essential. Far more than two-thirds of the 180 respondents’ businesses (78%) are currently finding it much more difficult or somewhat more difficult to obtain the necessary inputs for operations.

- The respondents were also given the opportunity to leave open comments. Overall themes in the comments demonstrate an understanding of measures to combat Covid-19, but also great concern about the current measures’ impact on businesses.

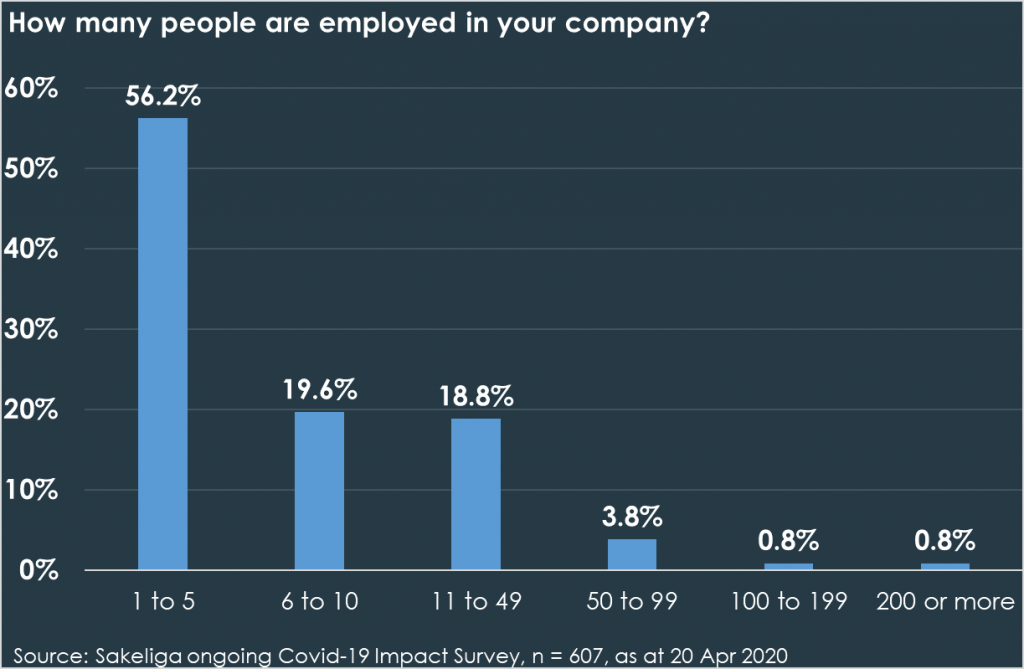

- The respondents were mostly from Gauteng and the Western Cape, and most of the respondents’ businesses, about 95%, employ fewer than 50 people. 607 respondents participated.

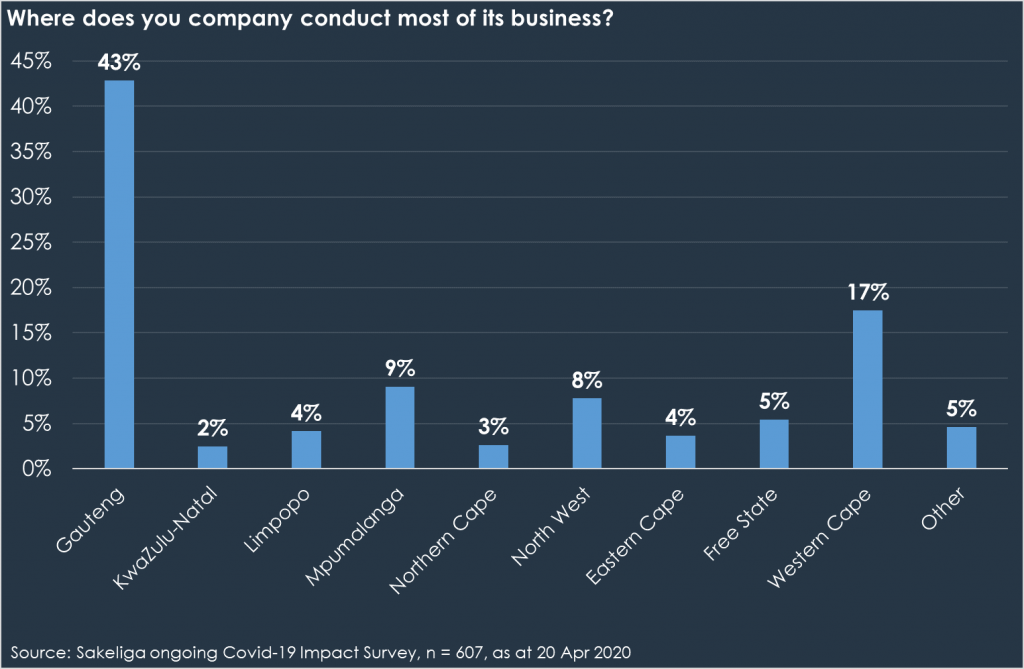

Survey Sample: Sakeliga circulated an email newsletter survey to its members and broader network. The first 607 respondents’ feedback was incorporated into this report. The survey commenced on 16 April 2020 and concluded on 20 April 2020. Out of the provinces, Gauteng (43%) and Western Cape (17%) were represented most strongly.

Almost 76% of respondents’ businesses had 1 to 10 employees, but 95% of all respondents are part of enterprises with fewer than 50 employees. Almost 13% of the respondents reported being part of an existing local chamber of commerce.

Covid-19’s short-term impact: According to some 82% of respondents, conditions over the relevant preceding seven days grew considerably worse (65,7%) or somewhat worse (16,1%) due to Covid-19 and the authorities’ reaction to it. For nearly 16%, conditions remained the same as before. Only a meagre 2,5% indicated better conditions than before.

Respondents were also asked to evaluate their prospects over the next 30 to 90 days (as opposed to “seven days before”) and after the next 12 months (as opposed to “today”).

30 AND 90-DAY PROSPECTS

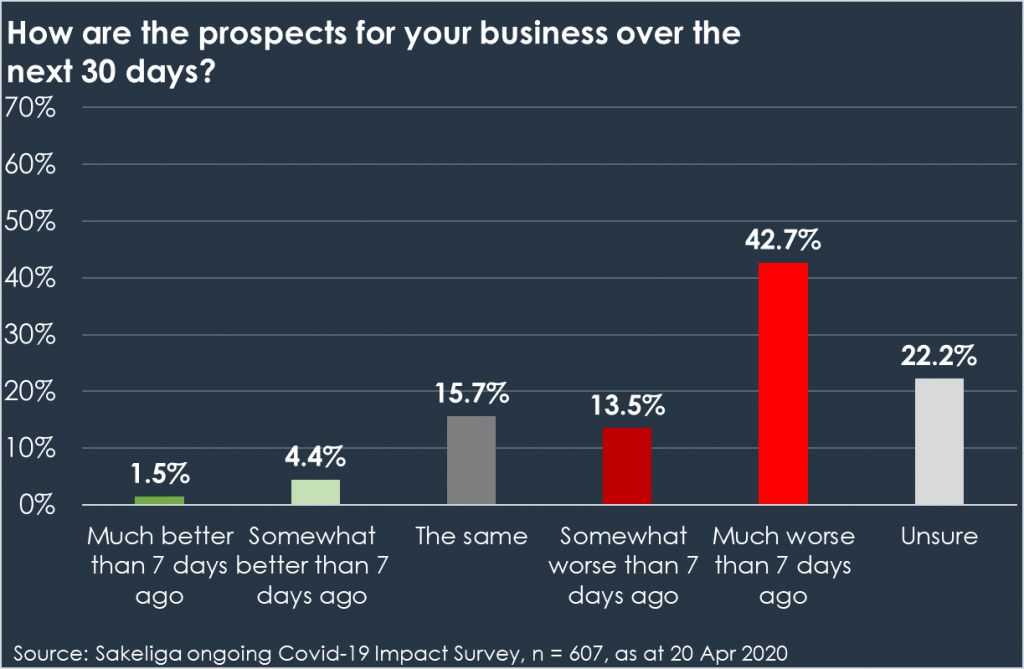

Prospects for the next 30 days: Around 56% of respondents indicated that prospects over the next 30 days are much worse (42,7%) or somewhat worse (13,5%) than seven days previously. 5,9% of respondents indicated much better (1,5%) or somewhat better (4,4%) prospects for the next 30 days. For 15,7%, prospects were the same, and 22,2% were undecided on their 30-day outlook.

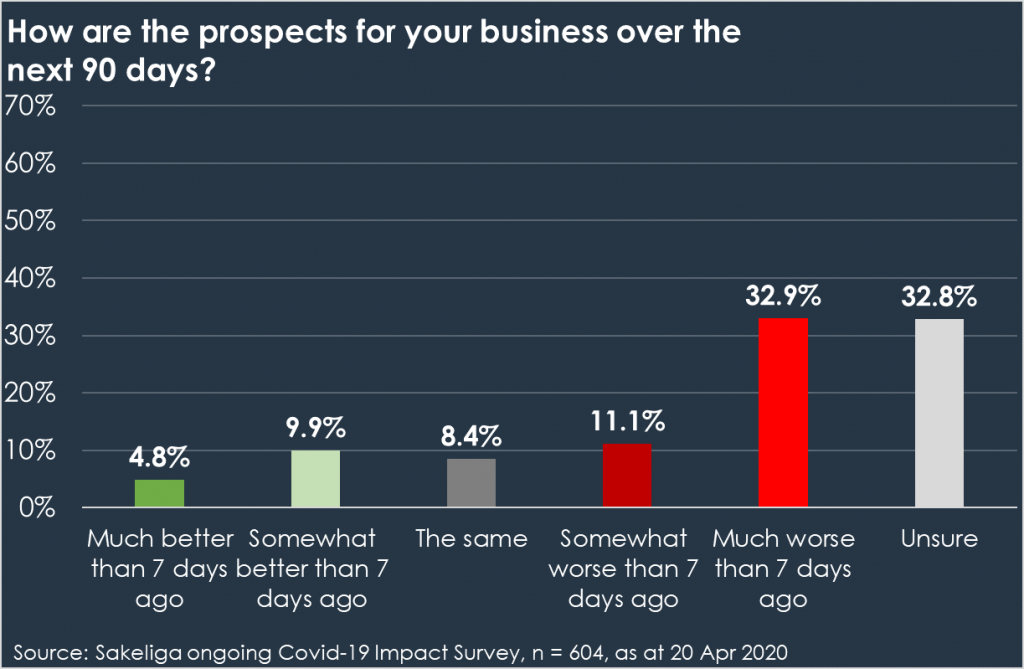

Prospects for the next 90 days: 44% of respondents indicated much worse (32,9%) or worse (11,1%) prospects for the next 90 days. In contrast to the 30-day outlook, uncertainty had increased (from 22,2%) to about 33% for the 90-day outlook. As for the 90-day outlook, nearly 15% of respondents expect much better (4,8%) or somewhat better (9.9%) prospects. Approximately 16% expect the same prospects.

Although the 90-day outlook is slightly better compared to the 30-day outlook, nearly half (44%) of respondents still expect much worse (32,9%) or somewhat worse (11,1%) prospects. In addition, a substantial almost 3 in 10 (32,8%) of respondents were uncertain about the 90-day outlook.

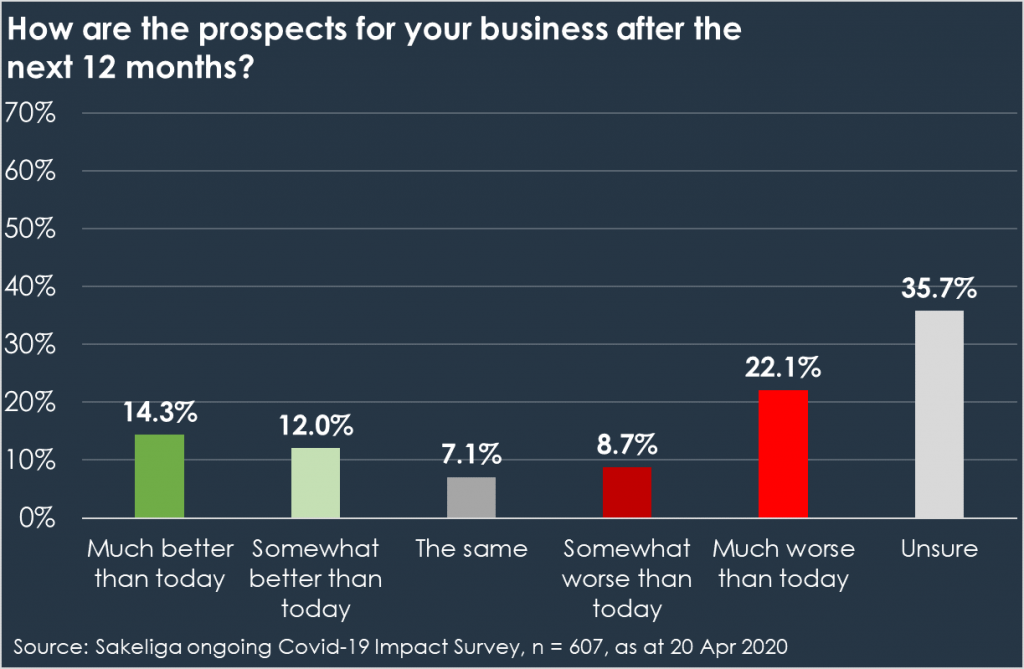

Prospects after 12 months: Respondents were also asked about their prospects after 12 months. Nearly 31% of respondents indicated worse (8,7%) or much worse (22,1%) prospects after the next 12 months. More than 26% of respondents indicated better (14,3%) or much better (12%) prospects, while around 36% were uncertain about their prospects after 12 months. Around 7% reported the same.

The above results still paint a picture of an extremely negative effect on immediate business conditions. Especially the 30-day outlook, but also the 90-day outlook, is predominantly negative. Moreover, uncertainty increases as the future outlook is extended. As for the 12-month outlook, more or less an equal number of people expect better and weaker prospects, but the outlook still leans more towards the negative.

There are indications that some business people’s outlook shifts from negative to positive as the future outlook is extended to the 12-month period – a potential silver lining. These trends will need to be monitored over time before definite conclusions can be drawn.

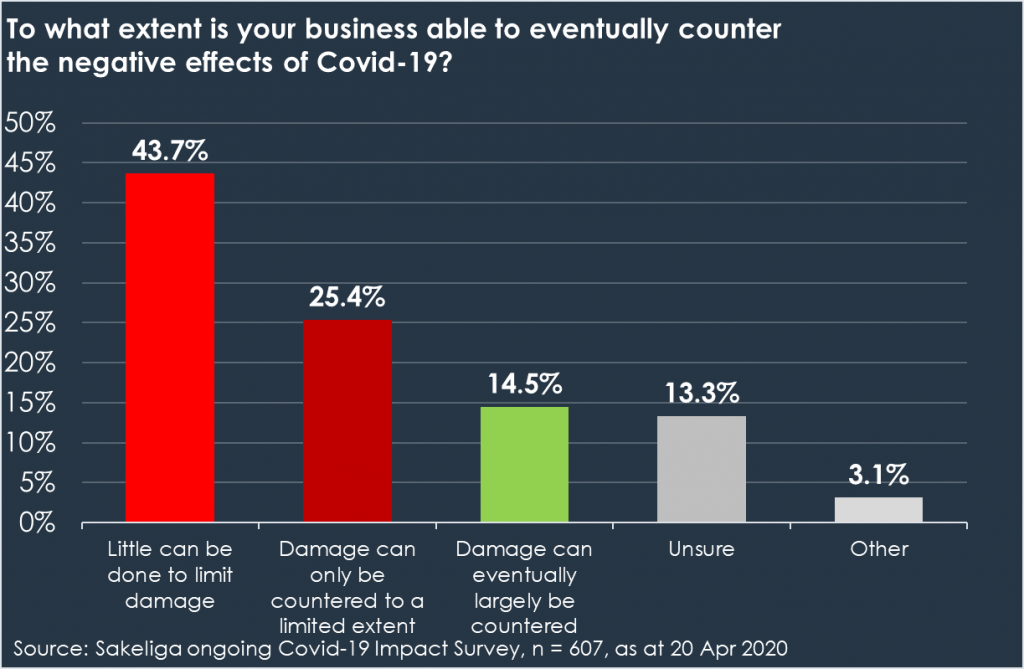

Extent to which Covid-19’s damage can be countered: The respondents were also asked to give their impressions about the extent to which they will ultimately be able to counter the impact of Covid-19 in their business. A worrying almost 44% of respondents felt that not much could be done to ultimately counter the damage. More than 25% felt that the damage would be offset to a limited extent. Only about 15% of the respondents expect the damage will ultimately be largely countered, and 13% were undecided on this (3,1% gave other feedback).

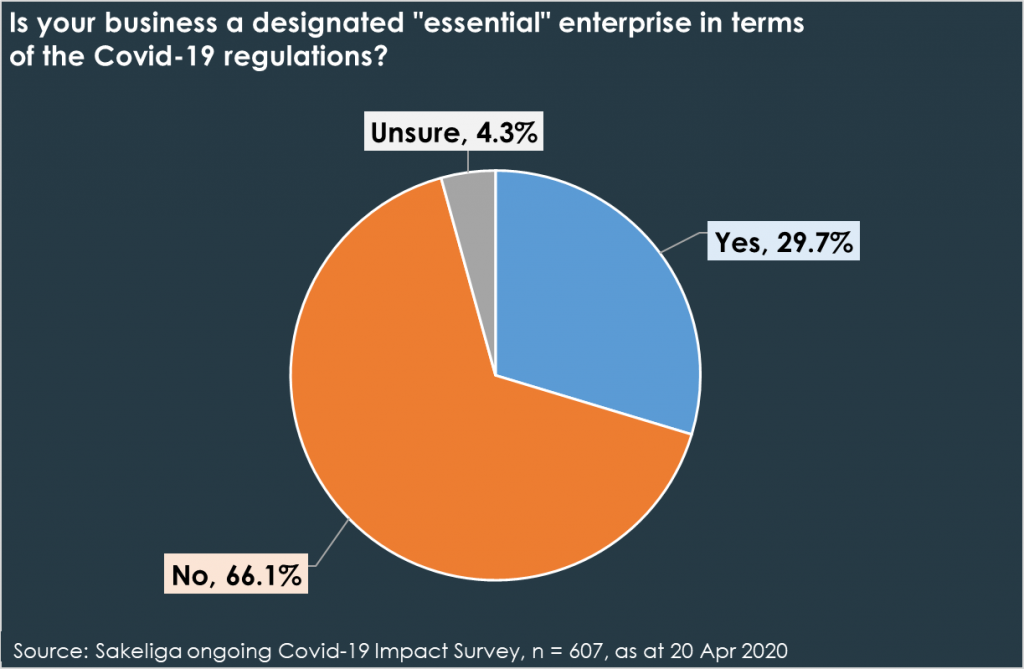

Essential businesses: In the survey, 180 (nearly 30%) of the 607 respondents indicated that the enterprises where they are mainly engaged have been designated as “essential”. A follow-up question was put to these 180 respondents to determine how easy or difficult it is in such businesses to obtain the necessary inputs for operations. About 78% of respondents in “essential” businesses indicated that it is much more difficult (50,6%) or somewhat more difficult (27,2%) to obtain the necessary inputs for operations. We emphasise that it is precisely the “essential” businesses that are highlighting such hurdles.

Expected impact on total sales (turnover): In the next question, all the (607) respondents were asked to give an indication of Covid-19’s impact on total sales (turnover) for 2020 as a whole compared with 2019. A disturbing about 62%, or nearly two-thirds of the respondents, expect a decline of more than 25% in their total sales (turnover). In total, an expected 87% of the respondents expect a drop in their business’s total sales in 2020 compared to 2019. The extent of the large expected declines that many of the respondents indicate is, however, very worrying.

Open comments: The respondents were also allowed to leave open comments. While more in-depth analysis is possible, the overall themes are an understanding of the measures of Covid-19, but also great concern about the current measures’ impact on businesses.

Ends.