")

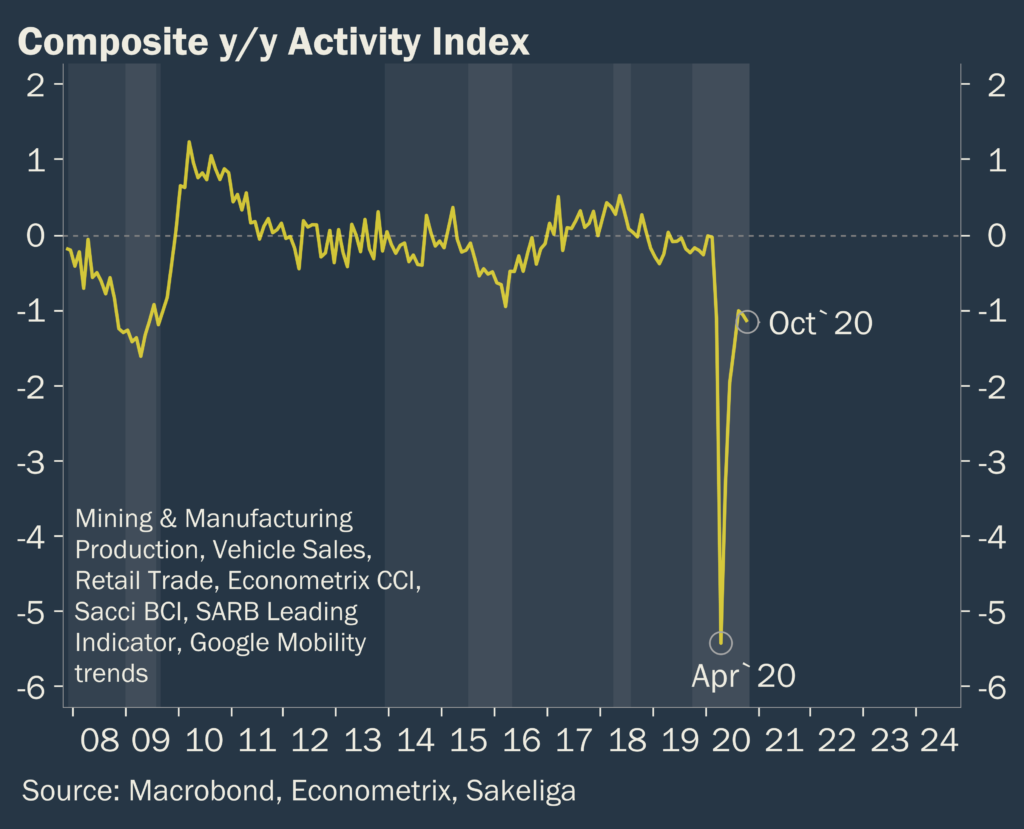

Various economic indicators are illustrating a difficult return to normal business conditions. New and lingering lockdown measures – locally and abroad – are likely to weigh down incomes and consumer confidence, which will hamper South Africa’s already frail recovery.

Many countries, especially in Europe, have reinstated lockdown measures. These measures are affecting travel and production and will increase pressure on South Africa’s frail recovery from hard lockdown of the second quarter of 2020.

This is according to the Sakeliga-ETM Economic Update for Business Decision-making released today. The November report considered local and global macro-economic trends relevant to businesses.

The main conclusion of the report is that economic activity and production, while recovering since the adverse levels of the lockdown, remain weaker than before. Lingering after-effects of lockdowns, Covid fears and supply disruptions are expected to constrain commerce for some time to come. This will hamper employment and investment and increase pressure on South Africa’s fiscal position.

While local production has somewhat recovered, household incomes remained under strain in the third quarter. Spending activity is partially supported by extreme low interest rates and large government deficits, neither of which reflect long-term economic health. Moreover, globally, recoveries are uneven and potentially unsustainable, which would pose a further drag on the local economy.

Sakeliga advises its members to remain vigilant on the possibility of new lockdown measures and tax increases and to be wary of asset expropriation risks in the face of market unfriendly policies and mounting fiscal stress. At this stage, the need for positive policy reform cannot be emphasised enough.

Read the complete report at the following link.

ETM-Sakeliga SA Policy Scorecard improves somewhat from very low levels

Despite enormous fiscal pressure, our ETM-Sakeliga Policy Scorecard has improved somewhat from 30/100 in Q2 to 40/100 in Q3. This largely reflects continued relative SARB prudence, recovering electricity output with more grid stability and better job market indicators since the Q2 employment slump.

The level of the index, however, still illustrates the evident lack of beneficial reform reflecting in the current administrations approach to economic policy.

About the Presidential Policy Scorecard

The index attempts to track a scorecard of the administration’s policy progress in terms of real-world effects rather than merely conjecture, promises, and wishlists. The scorecard comprises 10 factors, each scored out of 10 to make a score out of 100. We show an unadjusted and business cycle-adjusted index (using the ETM business cycle indicator). The adjusted index diminishes the effect of business cycle booms and recessions.

The 10 factors:

- The ETM labour market composite index (Stats SA, BER, SACCI)

- The rand vs emerging market currency basket exchange rate (Macrobond)

- South African bond yields relative to offshore bond yields (Macrobond)

- Political constraints on business survey (BER)

- ETM SA Fiscal Stress Index (Stats SA, National Treasury)

- Manufacturing fixed investment confidence (BER)

- SA vs emerging markets small & mid-cap equity performance (MSCI)

- Energy production (Stats SA)

- Net private investment/consumption ratio (SARB, Stats SA)

Net international investment position/GDP ratio (SARB, Stats SA)